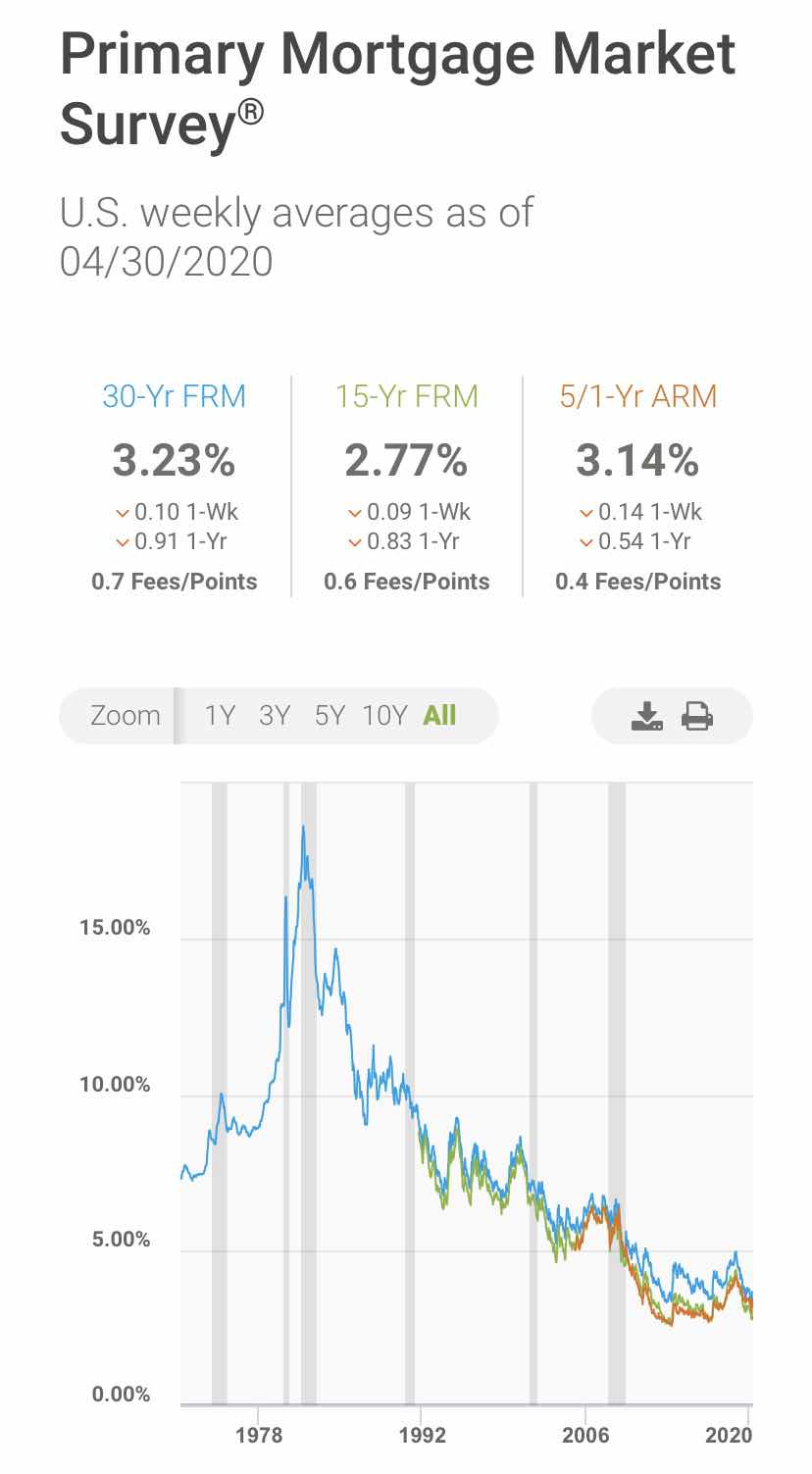

Well, let’s start with the facts first. As of today 5/3/20 the FHLMC 30 Yr Mortgage Prime Rate is still hovering at 3.23%! These are absolute historic low!! Throughout history, we, as a country, have never seen rates quite this low.. It’s UNPRECEDENTED, UNHEARD OF! Therefore, if you are in a position to buy a home, CEASE this opportunity!!! The low rates are producing high volume for refinances, which means, that if you need a job and have any type of real estate finance or mortgage experience, guess what? Banks are hiring!! They’re begging people to come to work with such high demand.

Second, this current market...it’s the new normal. Yup, you hear it right, there’s is No going back to the way things were. Who remembers the 2008 Mortgage Crisis Recession Crash? Banks have had 12 Yrs to learn from mistakes. They’ve spent this time making sure that their risk management practices were tough so that when a crisis like this hit, they’d survive. Bear Stearns and Lehman Brothers Anyone? Right, no one even remembers who they are anymore. The big banks aren’t sweating as much because they’ve spent all that time in the stance of “in the unlikely case of” scenarios.

Thirdly, Qualifying standards are tightening. On 4/11/20 JPMC announced that they would only approve loans with borrow who had a 700 Credit Score or Above. What does that mean for our Home Buyers? You will have to make sure your financial affairs are in line and order because the only way to get approval through this lender is having an A+ Credit Score.

Does that mean Buyers who have credit scores under 700 can't get approved? No, it just means they'll have to find a lender that services that market range.

Finally, the Sellers have had to make some adjustments. As Realtors we’ve added a new COVID-19 Addendum to extend contracts in case the virus has had an impact of the closing date being pushed out. Will your house still sell? Absolutely! It may just take a little longer than planned considering the current circumstances. If you are considering selling & haven’t listed the property yet, you may want to consider your states guidelines on the Shelter-In-Place Policy. This will have an impact of your final outcome. Your home will still sell. You just may need to exercise some patience in the process.